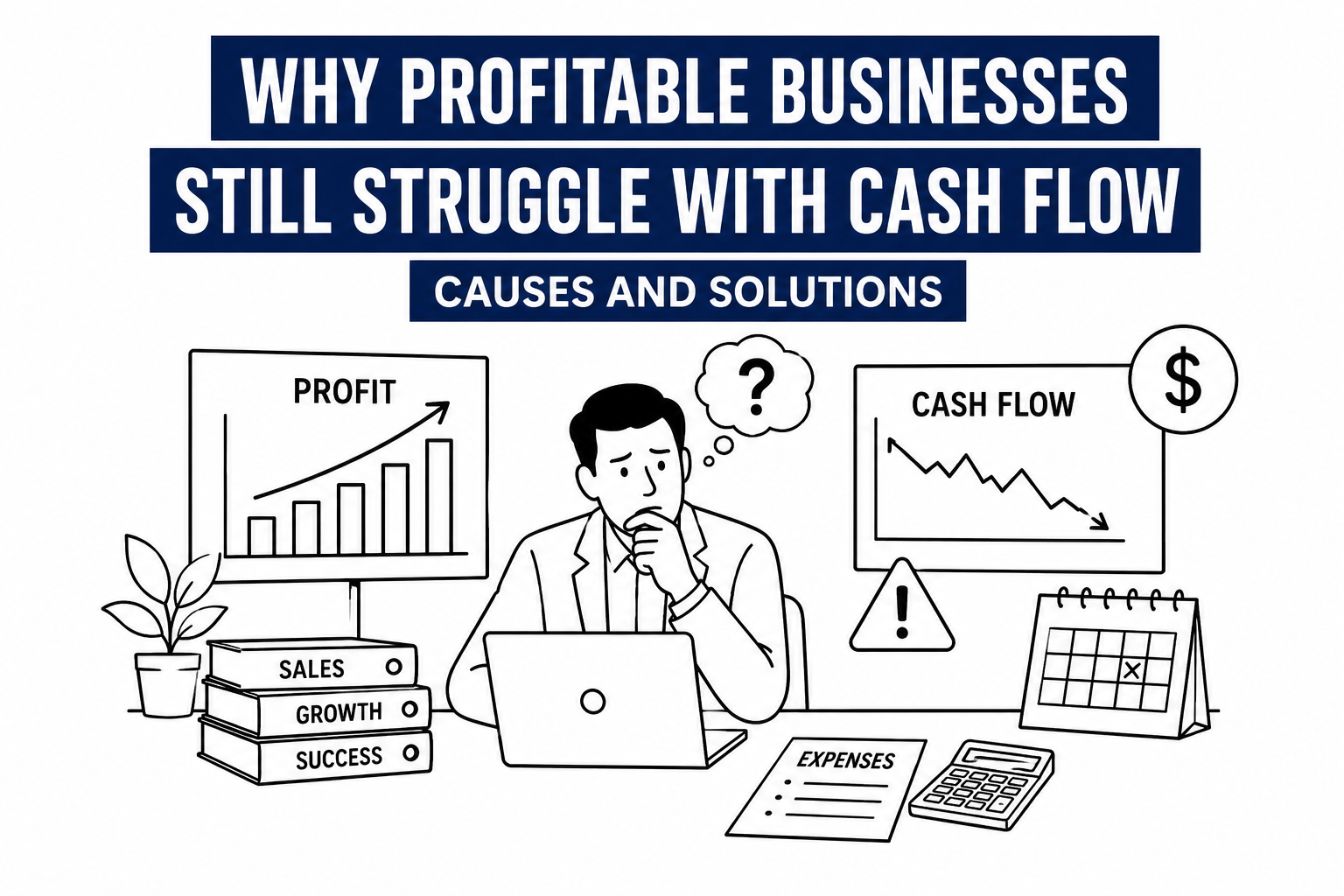

Why Profitable Businesses Can Still Face Cash Flow Challenges

Many business owners believe that earning a profit automatically means their company is financially secure.

However, profit and cash flow are not the same thing. A business may report impressive earnings while

still struggling to pay suppliers, employees, or operating expenses because there isn’t enough cash

available when it is needed.

Profit vs. Cash Flow

Profit represents the money left after expenses are deducted from revenue according to accounting rules.

Cash flow, on the other hand, measures the actual movement of money into and out of the business.

A company can be profitable on paper while experiencing cash shortages if customer payments are delayed

or cash is tied up in inventory and ongoing projects. :contentReference[oaicite:0]{index=0}

Common Reasons for Cash Flow Problems

1. Late Customer Payments

Long payment terms or overdue invoices reduce available cash. While sales may appear healthy,

the business cannot use money that has not yet been received.

2. Excess Inventory

Holding too much stock locks working capital into products sitting on shelves instead of keeping

cash available for day-to-day operations.

3. Rapid Business Growth

Growth often requires higher spending on inventory, staffing, marketing, and equipment before

additional revenue is collected. Without proper planning, expansion can create temporary cash shortages. :contentReference[oaicite:1]{index=1}

4. Poor Cash Flow Forecasting

Businesses that fail to monitor future income and expenses may be caught off guard by payroll,

tax payments, rent, or supplier invoices.

5. Large One-Time Expenses

Unexpected repairs, equipment purchases, tax obligations, or legal costs can quickly reduce available

cash even when the company remains profitable over the long term.

How to Improve Cash Flow

- Invoice customers promptly.

- Follow up consistently on overdue payments.

- Maintain healthy inventory levels.

- Create rolling cash flow forecasts.

- Negotiate better payment terms with suppliers.

- Build an emergency cash reserve.

- Review operating expenses regularly.

Final Thoughts

Strong profits are important, but they do not always guarantee financial stability. Monitoring cash flow,

planning ahead, and managing working capital effectively help businesses stay resilient during both growth

and economic uncertainty. Companies that balance profitability with healthy cash management are better

positioned for sustainable long-term success. :contentReference[oaicite:2]{index=2}